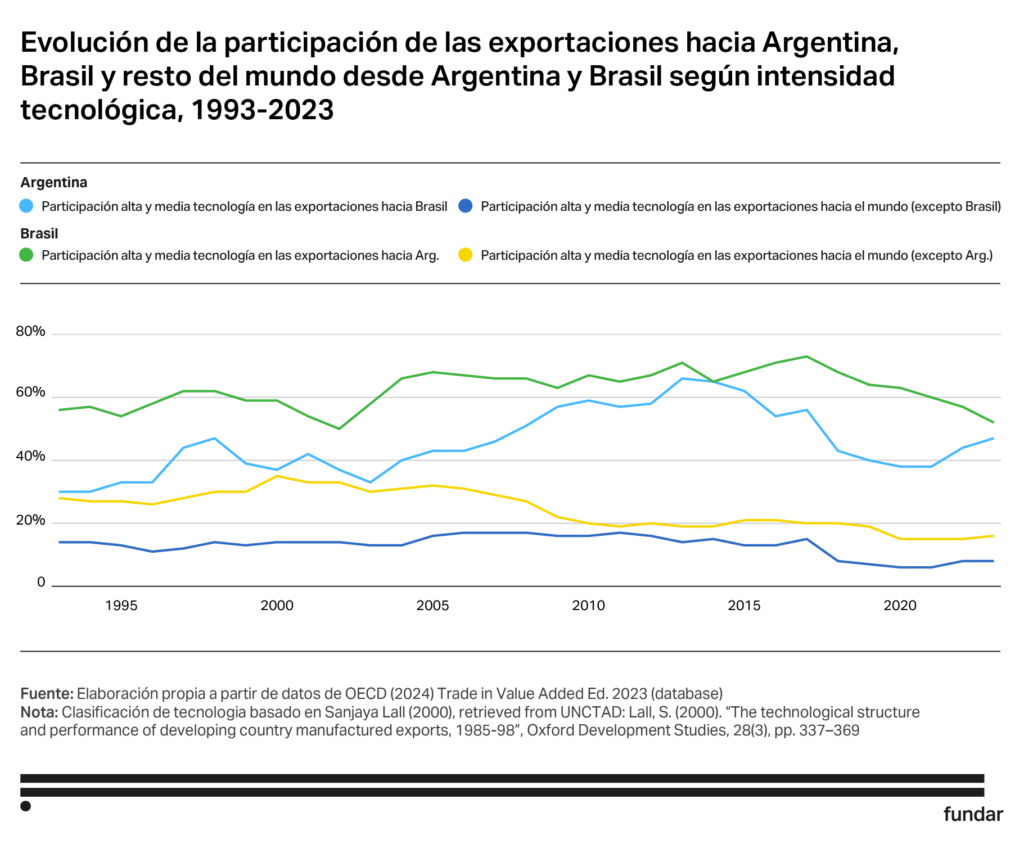

Productive integration between Argentina and Brazil is a key agenda item for productive development. Argentina exported US$66.788 billion in 2023, of which 17.7% went to Brazil. This amount is interesting in itself. However, its true relevance emerges in the composition of those sales: Brazil captured 56% of the country’s medium- and high-tech manufacturing exports.

Not only is Brazil important to Argentina, but—to a lesser extent—Argentina is also an important destination for Brazil’s more technologically complex exports. Argentina accounts for 5% of Brazil’s exports, but 15% of its sales of medium-high technology goods. These figures contrast with the process of primarisation or early deindustrialisation that both economies are undergoing. In the face of this process, the bilateral trade relationship maintains a small “island” of export complexity.

In this article, we seek to understand what lies behind this technologically complex export composition that characterises the Argentina-Brazil relationship and why it is important to strengthen it so that it does not collapse.

In collaboration with:

The growth of manufacturing exports and the formation of an island of export complexity

To understand this story, we need to go back to the 1980s. The shift from conflict to cooperation in the relationship between Argentina and Brazil had a resounding effect on the economies of both nations. The bilateral protocols signed by Argentina and Brazil between 1985 and 1991 established the initial mechanisms for productive integration and the reduction of trade barriers, leading to the formation of Mercosur, first with the Treaty of Asunción and then with the Protocol of Ouro Preto. The aim was to use regional integration as a mechanism that, replicating the European experience, would serve to increase the scale of regional production and then enable it to compete with the rest of the world. This trade was also intended to strengthen the bonds of peace and cooperation in the region.

The response was immediate. In a very short time, bilateral trade skyrocketed and there was a change in the export pattern of both countries.

The volume of trade grew and, in addition, there was a significant change in its composition, as shown in Figures 1 and 2. This process gave rise to what we refer to here as the “island of export complexity”.

From 1994 to 2013, there was an expansion in trade in manufactured goods to the region, while exports to the rest of the world continued to be dominated by primary products. However, industrial exports remained confined to bilateral trade and the Mercosur market, failing to expand to the rest of the world. This gave rise to an “island” of trade in manufactured goods with greater technological complexity between Argentina and Brazil.

In Argentina’s case, the expansion of manufacturing exports to Brazil in the period 2004-2023 was even greater than the expansion of primary product exports to the rest of the world, suggesting a significant transformation in production. In Brazil’s case, the expansion of manufacturing exports to Argentina during that period was profound. However, this leap was insufficient to sustain a major transformation in the overall export profile.

The sectors that led bilateral manufacturing export growth between 1994 and 2013 were those that were more mature, as a result of industrial developments during the import substitution period in the 1950s and 1960s (Teitel and Thoumi, 1986). In the case of Argentina’s exports to Brazil, the automotive industry played a leading role: it went from representing 18% of total exports in 1994 to 50% in 2013. Ten years later, with little change, it still accounted for 44% of total goods exported to Brazil. In Brazil, five manufacturing sectors maintained a high share of exports throughout the period: vehicles (24%), agricultural and combustion machinery (12%), processed iron and steel (7%), plastics and plastic products (6%), and electrical machinery (5%).

According to estimates from the Trade in Employment database, which links employment and trade data, there are nearly 300,000 Argentine workers associated with final demand for products in Brazil, and 450,000 Brazilian workers associated with final demand in Argentina (2020). All trade policy must take these data into account in order to assess the relevance of regional industrial integration.

Why did manufacturing exports to the rest of the world not increase significantly?

The problem with islands is that, being surrounded by water, they have poor connectivity. This network of manufacturing production and trade that was built between Argentina and Brazil did not produce a qualitative leap in the countries’ international integration. Neither Argentina nor Brazil managed to industrialise their global export profiles to a greater extent, unlike what happened in other regional blocs such as the European Union or ASEAN (Association of Southeast Asian Nations).

The functioning of regional value chains played a very important role in understanding these limitations. In both the EU and ASEAN, links in regional and then global value chains were the drivers of their export production leaps. In Mercosur, this development was asymmetrical and limited. Tariff policy, tax incentives and even geographical distance were also among the causes that led to the island’s isolation, but the role played by this limitation in the construction of regional chains is central to understanding the current situation.

Bilateral trade has been successful in maintaining its level of intra-industry complexity, but it has not been able to insert Argentina and Brazil’s high- and medium-tech manufacturing production into more complex regional chains in world trade. The pattern of integration was inward-looking—Argentina and Brazil, the two manufacturing centres, export industrial goods mainly to the region and not to third countries. Eduardo Viola and Jean Santos Lima (2017), from the University of Brasilia, have described Mercosur’s integration as ‘introspective’ which, unlike the Asian case, has been marked by high intra- and extra-regional protectionism, with trade in manufactured goods within the region itself and low export dynamism towards the rest of the world.

When analysing the composition of the value chains that make up binational productive integration, we find a very low rate of incorporation of Argentine inputs in Brazilian exports. Typically, Brazil prefers to use inputs from other sources. Thus, Argentine value added in Brazilian exports is only 3.49%. In the case of Argentina, the story is different: Brazilian value added in Argentine exports is 21.2%. The island has significant asymmetries.

Compared with the figures for the two largest economies in the European Union, these values suggest lesser regional power: Germany accounts for 14.9% of the foreign value added of France’s industrial exports, and France accounts for 7% of the value added of Germany’s industrial exports.

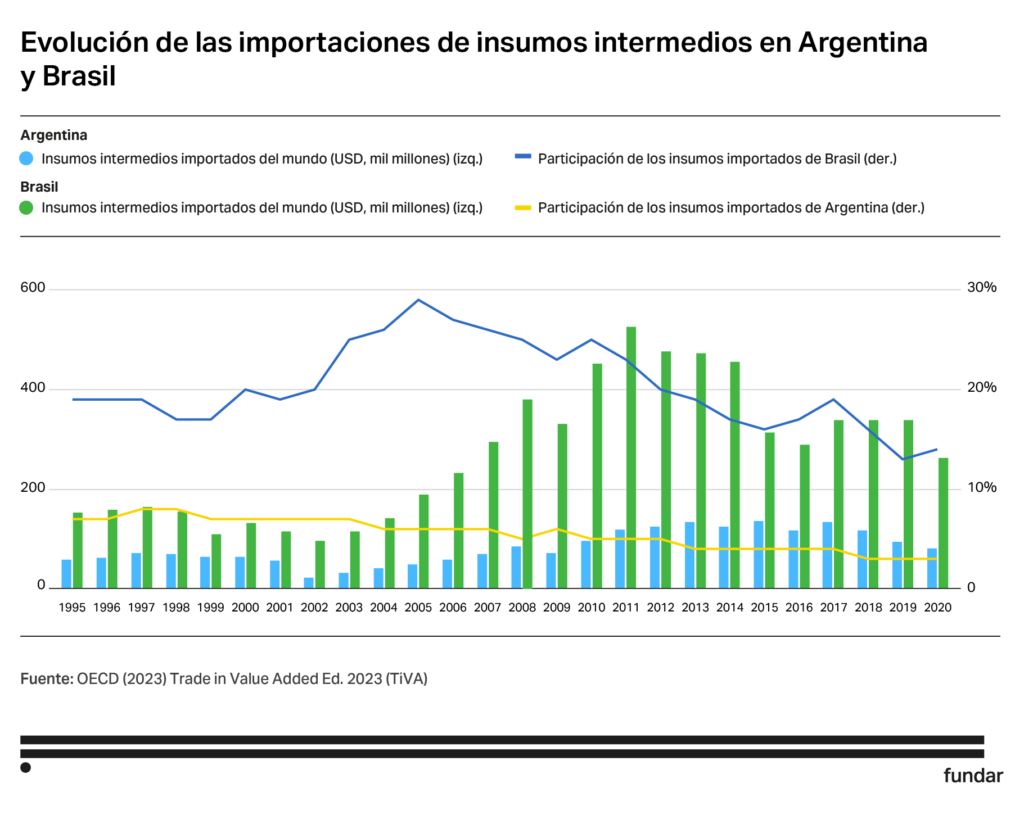

Despite initial integration success, these values have remained stagnant over the last 15 years and have even declined. While the amount of imports from around the world increased in both countries—from 20% in 1997–1999 to 25% in Argentina and 29% in Brazil— in 2018-2020—the share of both countries in total imported inputs fell by 5 p.p. in the case of Brazilian inputs used for consumption by Argentine industry and 4 p.p. in the case of Argentine inputs used by industry in Brazil. Recovering and increasing regional content is central to the reindustrialisation of the region.

Industrial production chains between Argentina and Brazil show a high level of divergence depending on the sector. While Brazil’s added value represents 37.92% of Argentine exports of basic metals and metal products, 26.52% of transport equipment and 22.47% of the wood and paper sector, other sectors show a lower proportion of Brazilian integration in Argentine exports, such as textiles (16.70%), plastics (14.82%) and chemicals and pharmaceuticals (14.11%).

On the contrary, Argentina’s contribution to Brazil’s industrial exports is more limited, both in terms of the sectors involved and in terms of magnitude. The main items include food, beverages and tobacco (6.68%), transport equipment (4.61%) and some other sectors with less than 3% integration. As mentioned above, Argentine inputs represent, on average, only 3.64% of the total value added of Brazilian exports, compared to 19.7% contributed by Brazilian inputs to Argentine exports. This asymmetry highlights an unbalanced structure in shared value chains, where Brazil plays a predominant role as a supplier.

The trade phenomenon between Argentina and Brazil shows an asymmetrical dynamic, evidenced by the evolution of imports of intermediate goods. While Brazil currently imports only 3% of Argentine intermediate goods—a significant drop from 10% in the late 1990s—there has been a significant change in its suppliers. China has increased its share from 3% in 2002 to 27% in 2022, displacing the United States, whose contribution fell from 28% to 14% over the same period.

In contrast, Brazil retains its position as Argentina’s main trading partner in imports of intermediate goods. It currently accounts for 24% of Argentine imports of these products, slightly down from 27% in 1996 and considerably lower than the peak of 34% reached in 2010. The entry of China as an industrial player in the region supplying intermediate inputs has mainly displaced the United States and European countries, whose combined share fell sharply from 42% in 1996 to 19% in 2022 (1).

Table 1: Production chains by industrial sector

| Industrial sectors | Brazil’s added value in Argentine industrial exports in 2019 | Industrial sectors | Argentina’s Added Value in Industrial Exports to Brazil 2019 |

| Base metals and metal products | 37.92% | Base metals and metal products | 1.74% |

| Transport equipment | 26.52% | Transport equipment | 4.61% |

| Wood and paper | 22.47% | Wood and paper | 2.48% |

| Non-metallic minerals | 18.64% | Non-metallic minerals | 2.25% |

| Machinery and equipment | 18.11% | Machinery and equipment | 2.32% |

| Electronics | 17.81% | Electronics | 1.41% |

| Petrochemicals | 17.42% | Petrochemicals | 1.40% |

| Food, drink and tobacco | 17.00% | Food, drink and tobacco | 6.68% |

| Textiles | 16.70% | Textiles | 2.47% |

| Others | 14.88% | Others | 2.36% |

| Plastics | 14.82% | Plastics | 2.78% |

| Chemistry and pharmacy | 14.11% | Chemistry and pharmacy | 2.81% |

Source: Fundar, based on data from TiVA-OECD (Ed. 2023).

Bolstering competitiveness, aligning incentives and building bridges so that the island does not sink

The island of export complexity, as we have seen so far, is valuable to national economies, but despite its importance, it struggles to stay afloat.

Competitiveness is a key component in this situation. It depends not only on microeconomic decisions made by industries, but also on macroeconomic factors that have shaped those decisions regarding industrial production. For example, currency appreciation, inflation—especially in Argentina—and high real interest rates—in Brazil—have hampered the ability of local companies to expand globally. As mentioned, Mercosur’s tariff and international negotiation policies and communications and logistics infrastructure have also limited the industry’s prospects in third markets and, in the long run, weakened competitiveness.

Recent political dynamics, with the decoupling of macroeconomic incentives, add an additional challenge to this scenario. The “Nova Industria Brasil” plan and the libertarian shift in Argentina, with instruments such as the Incentive Regime for Large Investments (RIGI), show that both countries are taking different directions in their economic plans. Brazil is committed to expanding its industrial production base, while Argentina is targeting FDI associated mainly with extractive industries. One point in common is that, curiously, neither has incorporated a regional perspective into its plans. Despite being each other’s most important industrial partners, there are no joint policies or attention to what is happening with the island of export complexity that is woven between the two nations. There is little intention to build bridges to keep the island afloat and connect it to the world.

Productive integration between Argentina and Brazil not only needs to return to a path that strengthens regional value chains, but also create strategies for joint integration into the global economy.

Currently, Argentina and Brazil have few trade agreements in place and face higher tariffs than their competitors and more complex technical barriers in their international integration. Even though tariffs affecting Argentine and Brazilian products are lower in industrial sectors than in agricultural sectors, they remain a factor in the projection of South American products to the rest of the world. For example, in the automotive sector, tariffs can reach up to 53% in some destinations.

Free trade agreements are an important tool on this path, but it is important to remember that they do not work on their own. It is necessary to accompany the productive sector in the process of international integration that these agreements open up and to create the conditions for Argentines and Brazilians to leverage each other’s global integration rather than competing with each other.

The island of complexity could be an oasis in the face of the region’s economic course. It is well worth taking a close look at how to keep it afloat.

(1) Trade estimates based on CEPII-BACI.

Bibliographical references

Teitel, S. y Thoumi, F. E. (1986). From import substitution to exports: the manufacturing exports experience of Argentina and Brazil. Economic Development and Cultural Change, 34(3), 455-490

Viola, E. y Lima, J. S. (2017). Divergences between new patterns of global trade and Brazil/Mercosur. Brazilian Political Science Review, 11(3), e0001.

About the Authors

Julieta Zelicovich – Researcher at Fundar

PhD in International Relations from the National University of Rosario and Master’s Degree in International Trade Relations from the National University of Tres de Febrero. Associate researcher at CONICET and lecturer in the International Relations degree programme at the National University of Rosario and in the Master’s Degree in International Politics and Economics at the University of San Andrés.

Nicolás Sidicaro – Researcher at Fundar

He holds a degree in Economics from the University of Buenos Aires and is pursuing a master’s degree in Economic Development at the National University of San Martín. He also specialised in Social Policy at the National University of Tres de Febrero. He worked at the Centre for Studies on Production XXI at the Ministry of Economy. He is a teaching assistant in econometrics at the University of Buenos Aires and UADE.

Master’s degree in Public Administration, specialising in Economic Policy Analysis, from Columbia University, and a degree in International Relations from ESPM. He has worked as a market analyst at a government agency for economic development and trade promotion, and as a consultant for companies at different stages of internationalisation.